Driver · 01

Smartphone adoption

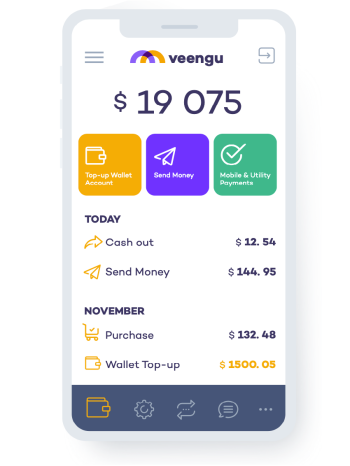

A pocket-sized branch the operator ships in days, not decades.

The Veengu platform allows you to run e-money and wallets, digital-banking mobile apps, and multi-currency wallets — from one cloud-native stack.

A neobank — sometimes called a challenger bank or digital bank — is a financial-services provider that operates entirely through mobile and web channels, with no physical branches. The product is the app: account opening, KYC, debit cards, transfers, analytics and customer support all live inside it. The infrastructure underneath is cloud-native by default.

A pocket-sized branch the operator ships in days, not decades.

Digital onboarding accepted by an expanding list of supervisors.

A generation that compares its bank to its messaging app.

Onboarding, products, channels, the integration layer, and everything around it — configurable per tenant.

Instant onboarding via mobile app or dashboard screens. Images and document flows.

Debit, prepaid, multi-currency accounts. Communities and corporate structures.

Send money to everybody within your platform. Involve people who are not involved with marketing transfers, bonuses and coupons.

Configurable workflows with third-party integration to support local AML and KYC regulations.

Multi-currency wallet, instant currency conversion with fair-consent user experience.

Integration with processors, payment providers, PSPs and payment aggregators.

Token-based integration with Paymentology and Network International. Virtual cards, Apple Pay and Google Pay supported.

Source-available iOS and Android apps published under your developer accounts. Customise the brand, the UX, the channel mix.

Veengu Dashboard with approval workflows, queues and exception handling. Granular roles and permissions for every operator role.

Configurable fees, limits, tiers and counters. Cashback, FX margins and membership pricing — per profile, per channel.

Operational dashboards plus deterministic end-of-day snapshots feeding regulatory reports. Audit trail covers every state change.

Multi-zone by design. No single weak spot — traffic shifts on zone failure with no end-user impact.

Most e-money projects require significant capital investment into heavyweight software platforms, infrastructure and vendor implementation services.

Veengu solves this problem. We offer an end-to-end 24/7 secure cloud service with ready-made mobile apps and portals for end-users, plus a back office for service-provider operations.

The platform was built to remove the recurring blockers that delay neobank programmes: long vendor implementation cycles, opaque pricing, brittle integration boundaries, and compliance retrofits late in the project.

Configurable feature packages turn most of the launch effort into operator decisions, not vendor change-requests. Greenfield deployments have gone from contract to sandbox in four to eight weeks.

Each engagement is quoted across four components — implementation fee and custom development as one-time costs, SaaS / licence and customisation maintenance as recurring — with capacity scaling already built in. Full first-year launches typically clear the USD 70K floor and grow with the operator, not with seat counts.

KYC orchestration, configurable workflows, immutable audit trail, regulatory-reporting outputs, and tokenised card-data handling — compliance posture you can defend at audit.

Ten-plus customer deployments in production, including a single tenant carrying more than five million accounts. The same platform you launch on is the platform you grow on.

Pick the modules you need today — wallets, cards, transfers, agent network, FX, business-process automation — and add the rest as your roadmap matures. Each module is configurable per tenant.

White-label apps published under your store accounts, REST API for your own front-end builds, and an optional source-code handover so you can fork your own product when you are ready.

Tell us about your project — regulatory licence, target geographies, expected scale, integration constraints. The more concrete the scope, the faster we come back with a quote and clear next steps.

We respond within three business days. Inquiries with a clear regulatory licence, target geography and integration list move fastest.

A comprehensive software suite for different verticals in financial services, configurable to implement your vision with our platform and professional services. Build unique fintech solutions across the world with our modular, cloud-native platform.

Veengu empowers financial institutions with cutting-edge tech solutions. Build unique fintech offerings across the world with our modular, cloud-native platform.

Individual and merchant wallets. Marketplaces. Electronic money.

ReadSoftware stack for licensed electronic-money institutions.

ReadAgent networks, USSD / app channels, cash-economy use cases.

ReadSource-available wallet app for fast brand launches.

ReadMulti-party orchestration with online FX and compliance.

ReadWallets and payment instruments inside non-fintech products.

ReadOperators that built digital-banking propositions on Veengu — transformations and greenfield launches both.

A wallet operator transitioned to full digital banking under regulator oversight — running on the Veengu core through the migration and after.

A new wallet launched from scratch for a Caribbean market — onboarding, accounts, payments and an agent network on day one.

A digital onboarding flow for merchants — wallet-led, mobile-first, signed off by the supervising regulator.

Whichever solution you launch, you launch on the same Veengu platform. These are the modules a typical operator turns on.

Profiles, accounts, balances, immutable postings.

ReadLedger, postings, settlement, end-of-day cycles.

ReadMulti-tier KYC, progressive limits, audit trail.

ReadSource-available reference apps for mobile, web and agent.

ReadToken-based integration with card issuers.

ReadMulti-zone by design.

ReadVeengu provides modular core-banking and payment-orchestration technology for regulated digital financial services — across the Middle East, Africa, and beyond. We do not provide financial services, payment processing, or regulated fintech activities; we provide the software an operator runs to do them.

A neobank — also called a challenger or digital bank — is a financial-services provider that operates entirely through mobile and web channels with no physical branches. The product is the app: account opening, KYC, cards, transfers and support all live inside it, on cloud-native infrastructure.

Not necessarily. Operators typically choose one of two models: licensed, where the operator holds its own banking, EMI or payment licence; or partnered, where a sponsor bank or BaaS provider holds the licence. Veengu supports both — the platform sits behind the operator regardless of where the licence lives.

Digital onboarding, debit and prepaid multi-currency accounts, card issuing with virtual cards plus Apple Pay and Google Pay, transfers, FX, a configurable pricing engine, white-label banking apps, an operator back office, and reporting with an audit trail over every state change.

Configurable feature packages turn most of the launch into operator decisions rather than vendor change-requests; greenfield deployments have gone from contract to sandbox in four to eight weeks. Pricing depends on use case, integrations, deployment region and scale, with full first-year launches typically clearing a USD 70K floor and growing with the operator rather than with seat counts.

Yes. Veengu has 10+ fintech installations in production, and one of the largest customer deployments runs beyond 3M individual end users and 6M accounts. The same platform you launch on is the platform you grow on.

Bring your regulatory licence, target geographies, expected scale and integration constraints. We respond within three business days.